Setting up your Auto Insurance Owning a vehicle is one of the basic parts of being a member of American society. Getting a car means mobility, and mobility means freedom! Along with that freedom comes responsibility: the responsibility to look out for your fellow motorists. While most agree that being responsible is the right thing to do, all fifty states have put financial responsibility laws that apply to motorists on the books. There is more to insurance, however, than just “having it” or “not having it.” There are different levels that a savvy motorist should know about it. LIABILITY INSURANCE Liability insurance, as mentioned before, is required in all fifty states for any vehicle on the road. Liability is expressed in the following format: 50/100/50. What that means in plain English is, if you have these levels on your auto insurance, you have $50,000 worth of insurance for Bodily Injury for one person, $100,000 for the whole accident for Bodily Injury, and $50,000 worth of insurance for Property Damage. While the Property Damage portion could apply to any type of property damage you cause in your vehicle, it usually means “the other guy’s car.” It’s important to realize that liability insurance applies to “the other guy,” not your car. If you are in an accident, and it’s your fault, your liability insurance will pay for the other person’s losses, up to the policy limits, but you are on your own. This leads us to the next level of insurance. FULL COVERAGE This term gets used quite a bit in the insurance trade, but there is actually no such thing as “full coverage,” since there is no way that every single cause of loss could be covered. What it usually means, however, is someone has liability, comprehensive, collision, and uninsured motorist. Some people also include fringe coverages like roadside service and rental car reimbursement in the term full coverage. “Full coverage” insurance is most often used in the context of providing coverage for the vehicle in the event of theft, collision, or unexplained damage to the vehicle. Banks that give loans on cars require that vehicles on which they hold the note carry full coverage. Their logic is, they want to make sure that they can get their portion of the investment on the vehicle back in the event of a loss. While “full coverage” is not necessary to drive legally, it makes sense in many cases, especially when the insured does not have the resources to buy another car in the situation in which the car is destroyed or stolen. Fringe coverages, while also not required, can make life much easier in the event of a loss. To find out what coverage meets your life situation, it is best to sit down with an experienced, licensed insurance agent to go over your particular situation to see what makes sense for you. While I hope you find this information useful, this does not replace advice given by an agent with first knowledge of your life situation. If you would like to discuss your personal situation, please feel free to contact me via email at dave@thedaveowens.com or you can call me or my licensed staff at (661) 946-4224. We’d love to hear from you!  Dave and his daughter Kate

0 Comments

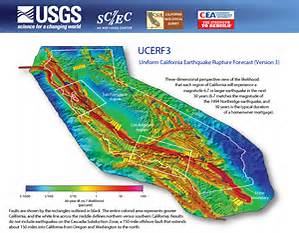

http://www2.earthquakeauthority.com/ On October 3, 2016, the LA Times wrote an article about how homeowners in California are taking risks by not having earthquake insurance. In fact only 17% of all California homeowners have earthquake insurance. In this blog I will share with you the benefits of having earthquake coverage and if this coverage is best for you. For anyone who has lived in Southern California for any length of time, you know that this is Earthquake Country! In fact, a little shaking of the ground barely generates a comment from locals! It has to be a fairly large earthquake to get our attention! That being said, earthquakes are no laughing matter. A casual observer can see hairline stucco cracks radiating out from windows in homes of even fairly recent construction. While our homes in Southern California are designed to be earthquake tolerant, they are NOT earthquake proof! One of the most common questions I am asked as an insurance professional is, should I purchase earthquake insurance for my home? The answer to this question is not a pure “yes” or “no,” but each individual situation needs to be examined. While only you can make the right decision on purchasing earthquake insurance, I will give you a few thoughts to consider. First of all, the big player for earthquake insurance in California is the California Earthquake Authority, or “CEA.” Admitted insurance companies (those who have been licensed by the California Department of Insurance) who sell homeowner’s insurance are required to offer earthquake insurance through the California Earthquake Authority. In fact, insurance buyers are required to sign a form saying that they were offered earthquake and that they chose not to purchase it. That’s how important the State of California views earthquake insurance. In addition to the CEA, there are a number of other companies that offer earthquake insurance as well. They often offer earthquake insurance for larger risks like apartments or retail buildings. With that introduction to the earthquake insurance market, the question remains, “should I buy earthquake insurance?” In my opinion, the main concern you should have is another “EQ” word, and that word is “equity.” Equity is the value of your home, minus any financial encumbrances you have on it. In other words, the value of your home minus the mortgage. For several years, many people had negative equity, or they were “upside down” on their home: they owed more than the home was worth! For someone in an “upside down” situation, purchasing earthquake insurance may not make sense. The reason for this is, if an earthquake were to occur, the purchaser could still very well find themselves without a home. They purchased insurance on their home, but after the deductible is factored in, all of the money goes to the mortgage company, and the homeowner does not have the means to rebuild! The earthquake policy ended up leaving them in a worse position because they paid premiums for a policy that provided them little to no benefit. On the other hand, someone who has a substantial amount of equity should seriously consider purchasing earthquake insurance. When you have a mortgage on your home, you and the financing institution share ownership of the property. As you pay down your mortgage, your share of the ownership goes up, the bank’s goes down. The amount of money that needs protecting goes up as the years go by. We are currently seeing a rise in property values which is speeding up the increase of values of homes. You may very well have gone from “upside down” to very well placed value-wise in a very short period of time! If you are in this position, a visit with your insurance agent is probably in order. Earthquake policies are structured differently than regular homeowner’s policies. Rather than having a set dollar amount of a deductible ($1000, $2500, etc.), the deductibles are set as a percentage of the total rebuild cost of your home. Currently, the CEA offers a 15%, 10%, and very recently, a 5% deductible. How it would work is, if your home costs $300,000 to rebuild the deductible would be $45,000 if you were to have a 15% deductible. If you were to purchase a policy with a 10% deductible, you would pay $30,000 out of pocket. This high deductible has kept many people from purchasing a policy, and that reticence is certainly understandable based on the scenario I detailed above. The logic in purchasing an earthquake policy if you have equity in your home, even if you do NOT have the $45,000 to rebuild is that you would at least get SOMETHING out of your home. If you had $150,000 worth of equity, and you had $45,000 as your deductible, you could still potentially get over $100,000. Without the coverage, you get nothing. People often ask about whether or not the Federal government would help out in that situation. While I’m not disparaging the hard-working people of FEMA, the assistance provided by the Feds was variable at best. Using FEMA as your sole hope for insurance is probably not a good idea. As I said before, purchasing an earthquake policy is unfortunately not a black and white issue. It takes thought and information: something that our office can provide. If you are struggling with whether or not to purchase earthquake insurance, give our office a call. You can reach us at (661) 946-4224, or you can email me at dave@thedaveowens.com. I or my licensed staff will be happy to go over the “ins and outs” of earthquake insurance. I would also strongly suggest that you check out the following website http://www.shakeout.org/california/ for information on how to get prepared for the “Big One.” Whether or not earthquake insurance is right for you, every family should have an earthquake disaster plan, and this site can help you be prepared.  Dave Owens and his daughter Kate  Protecting your business After years of recession, it appears that the economy is moving forward. Some would say that we are back in a prosperous position, some people have decided that starting up a business is a great way to make money doing what they love. Many folks have a dream of owning a restaurant, or perhaps opening a mechanics shop. They are learning the “ins and outs” of a business plan and laying the groundwork for their future as their own boss. If you happen to be one of those people, you can’t leave insurance out of the mix. Many small businesses fail in the first year because they didn’t take insurance into account. They suffered a loss, and because they didn’t have insurance, they did not have the resources available to get back in business. Don’t let this be you! Following is a list of five types of insurance that you need to consider when opening a business. 1) Property and Casualty Insurance. Property and Casualty insurance is the cornerstone of any insurance program. When you become a business owner, the world looks at you differently. Instead of being “Dave the ‘Working Stiff,’” you are now “Dave the Business Owner.” Some people think that since you own a business, you must be “rolling in the dough!” Most business owners KNOW that this is not the case, but we’re talking about perception. You are now a bigger target for people who want to make a quick buck from insurance. Staged accidents, especially in retail establishments, are not as uncommon as you might think. The liability portion of your Property and Casualty policy covers you against these types of “accidents” as well as the true accidents that we all want to avoid. Also, if you are opening up a retail business, there is usually a tremendous amount of inventory and equipment involved. You need to protect your investment in case you are broken into and robbed, or in case the place of business burns down. Once again, it happens more often than we’d like to think. There are many other parts of a standard “business owner’s policy” or “BOP.” Check with a licensed agent experienced in business insurance to get more details. 2) Workers’ Compensation Insurance. Workers Compensation insurance covers your employees in the event that they are injured while working for you. This even includes people you pay on a 1099 basis if they work on an hourly basis using your equipment. A major injury by one of your employees, while devastating personally, will devastate TWO families if there is no Workers Compensation Insurance: your family, and your employee’s family. Don’t skip this vital coverage. 3) Professional Liability Insurance. Many businesses in which advice is given require professional liability. That includes real estate agents, financial advisors, as well as insurance agents. Counselors and tax preparers also often need professional liability to do business. This coverage is important in that it provides coverage to the professional in case they make a mistake in some way. Being human, we all make mistakes, even when we do our best to avoid them. This coverage can give you peace of mind as you work hard to grow your business. 4) Product Liability. Most liability policies cover this type of insurance loss. It is also sometimes “Products and Completed Operations” coverage, or PCO. This coverage is important in that it covers the business in the event that a product that they produce, or a service provided causes damage to someone with whom they do business. For example, an oil changing station changes the oil for a customer, but doesn’t put the oil plug back in properly. As a result, the oil drains out and causes the engine to burn up. PCO coverage would pay to replace the engine. 5) Business Interruption Insurance. This type of coverage can mean the difference in staying in business, or going out of business after a loss. Without this type of coverage, a business owner may be made whole in all of their inventory that is lost, but because it took a long time to rebuild, or to purchase new equipment or inventory, all revenue produced by the business comes to a halt. Many businesses could not afford to be on hold for two to three months. Business Interruption Insurance reimburses the business for income lost after a loss. Navigating through the complexities of business insurance can be a challenge. A small hole in coverage could leave a business in dire straits if left uncovered. For this reason, it is important to have an insurance professional to guide a new business owner in what type of insurance is necessary for them. Our office is experienced in helping new business owners get the coverage they need at a price that’s right. Feel free to call me or my experienced staff at (661) 946-4224, or email me at dave@thedaveowens.com.  Dave and his daughter Kate  Celebrating the 4th of July in a safe and thoughtful fashion  The Fourth of July weekend is coming up! This year, it's extra fun because, since it falls on a Monday, many folks get a three-day weekend. Lots of people will be traveling out of town, having barbecues, hitting the swimming pools, and attending local patriotic community events. One of the main things that almost all Americans associate with the Fourth of July is fireworks. In fact, our Founding Fathers suggested fireworks as a way to celebrate Independence Day so it has a long tradition in Americans' celebration of the Fourth of July. In addition to having lots of fun on the Fourth, there is a difficult side that many first responders will share with you. For firefighters, the increase in accidental fires caused by the misuse (and even proper use!) of fireworks goes up. Many have to give up the holiday because the departments need extra people on hand to take care of the increase in fires. Insurance claims go up due to fires as well. In addition to the fire danger, there are numerous injuries related to fireworks that occur during this time of year. Local emergency rooms see numerous burn injuries over the holiday, and even loss of digits as a result of misfiring fireworks. A little known fact is that 57% of injuries to children from fireworks come from sparklers. Many people don't realize that sparklers can generate up to 3000 degrees Fahrenheit: almost as hot as some of the cooler places on the sun. It's never a good idea to hand something that emits sparks to a three-year old child! Also, many pet owners (my family included!) really struggle through the Fourth of July and New Year's Eve. The reason is, the high-pitched and unexpected noise associated with the fireworks severely frightens dogs and other animals. Last New Year's Eve, my wife and I saw a poor dog running in the middle of the street in terror because of the fireworks. He ran out into the desert trying to get away from the noise. We don't know what happened to him. If this is a problem for you, a visit to your veterinarian may be in order. They can prescribe medications that can help your pets get through this time of year with the least amount of distress possible. Also, those who work with retired military servicemen and women who experienced combat will tell you that many of them struggle with this time of year because the fireworks bring back memories of combat. They often visit counselors knowing that it will be a difficult time. With all of this said, there are many, many ways to celebrate the Fourth of July in style without causing undue stress and hardship on our neighbors. Local social clubs and charitable organizations host pancake breakfasts featuring patriotic sing-a-longs and speeches. Many municipalities and sports teams host fireworks shows at their arenas which can be visited and even enjoyed for miles around. Bottom line, when you enjoy your time off, be aware that fireworks, while certainly beautiful and fun, can cause problems for our friends, neighbors, and pets. From my family to yours, have a safe and fun Fourth of July!! As always, feel free to contact us at 661-946-4224. We would be happy to help you with your Insurance needs.  Dave Owens and his daughter Kate  Fire season in Southern Califonia Fire season in Southern Califonia Today is the first day of summer and fire season is in full swing. As part of our continuing series on “what to do if,” today we will discuss, “what to do if you are ordered to evacuate by the Fire Department, Police Department, or local authorities.” While many people living in more developed areas will hopefully never have to deal with this situations, folks that live within a mile or so of areas that are experiencing fires may very well be ordered to evacuate. This exact situation happened to several of my policyholders during the Station Fire, and it has happened numerous times throughout recent history. Leaving your home due to fire or some other reason can be very traumatic for all involved, especially if you have young children. The uncertainty of what to take, what to leave behind, etc. can leave a family paralyzed with doubt and fear. Sometimes, people refuse to leave. This is a very, very bad idea. This is a bad idea for several reasons. First of all, their presence creates an extra burden on the authorities responsible for putting out the fire. They may possibly be required to commit extra resources to protecting that family, and leave other people or other people’s property unprotected. Also, if the situation becomes dire, the option of getting out may not be available. There have been many, many situations in which people who refused to leave their homes ended up losing their lives as well as their property. This is a tragic situation that could easily be avoided. Another reason that some people give when they refuse to leave their home is that they don’t know where they will stay. This is where having a good insurance agent, and good policy, come in. Most of the major insurance companies have a provision in their policies that will provide Additional Living Expenses (ALE) coverage in the event of an ordered evacuation. Your insurance policy will provide the additional costs associated with being away from your home, such as food, shelter, and clothing. What’s especially amazing about this coverage is that there is often NO DEDUCTIBLE! Additional Living Expenses coverage pays first dollar. Another way in which you can feel secure in leaving your home is that insurance companies respond to fires in much the same way that first responders do in that they identify areas that need resources and respond appropriately. Farmers Insurance, for example, has a sophisticated system of claims vehicles placed throughout the United States so that they can be up and running and serving policyholders within 12-24 hours of an identified event. In fact, Farmers is often the first insurance company on the scene and helps other insurance companies assist their clients. In the event of a catastrophic event, insurance companies generally work together to make people’s lives a little more bearable. So to recap, if you are ordered to leave, the best course of action is to….leave! If you live within a mile or so of a brush area, it would probably be wise to have a pre-packed “grab bag” that you can grab and go, depending on how much time you have available. If you have your “grab bag” already packed, and you have an hour to evacuate, you can then devote time to packing the irreplaceable items like family mementos, pets, or even some high value items that may be difficult to replace. If you live in horse country, the authorities will often direct you to the location where you can take large animals. It may also be a good idea to find a fellow horse owner BEFORE the fire who can temporarily board your animals. During fire season, be wise. Remember, there’s nothing in your house worth risking your life, or the lives of your loved ones. Get to a safe place, then call your insurance agent. I hope that this information has benefited you. This blog entry is not intended to replace advice on your specific situation. Contact an insurance professional to see how your specific situation may be addressed. You may also call me or my licensed staff at (661) 946-4224. You can also email me at dave@thedaveowens.com. Be safe!!  Dave Owens and his daughter Kate |

AuthorDave Owens, Owner/Agent. I have proudly served in the Insurance Industry for over 20 years. Archives

October 2019

Categories

All

|

RSS Feed

RSS Feed